Inflation Accumulation

Inflation Accumulation

Inflation is more than just a year over year comparison of price levels. It has long lasting implications for societal spending power and the overall wealth effect.

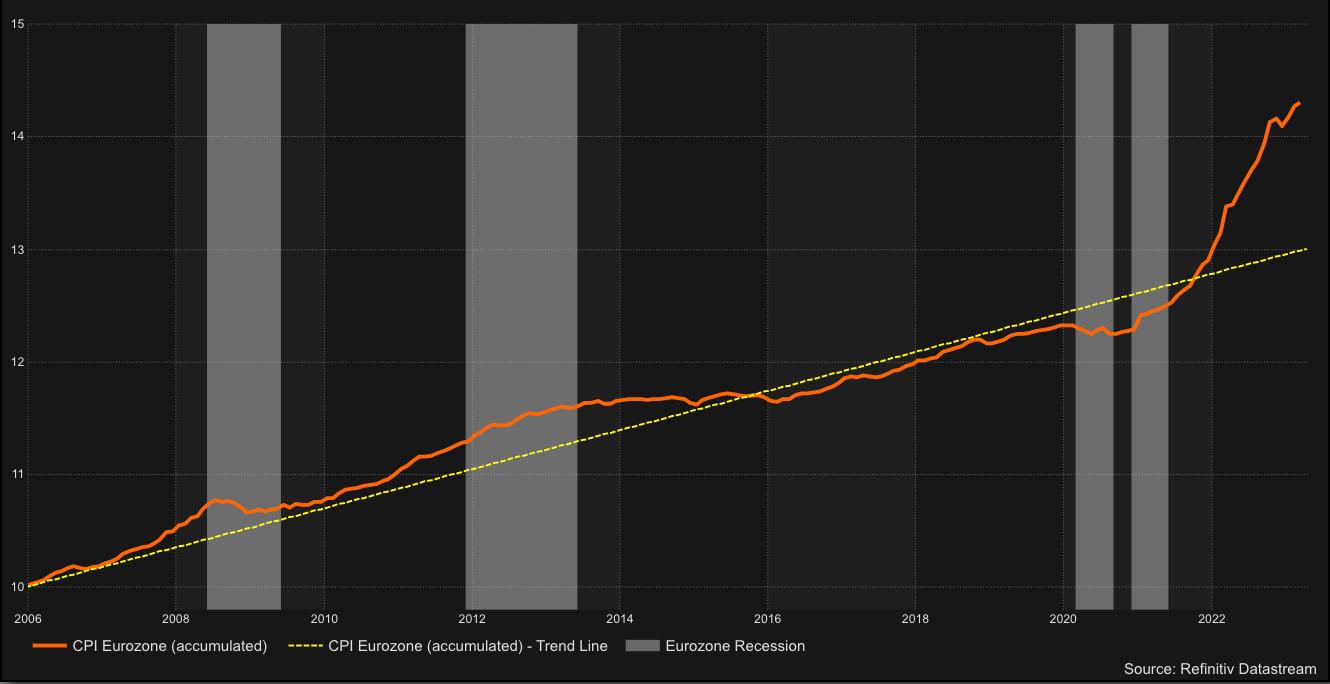

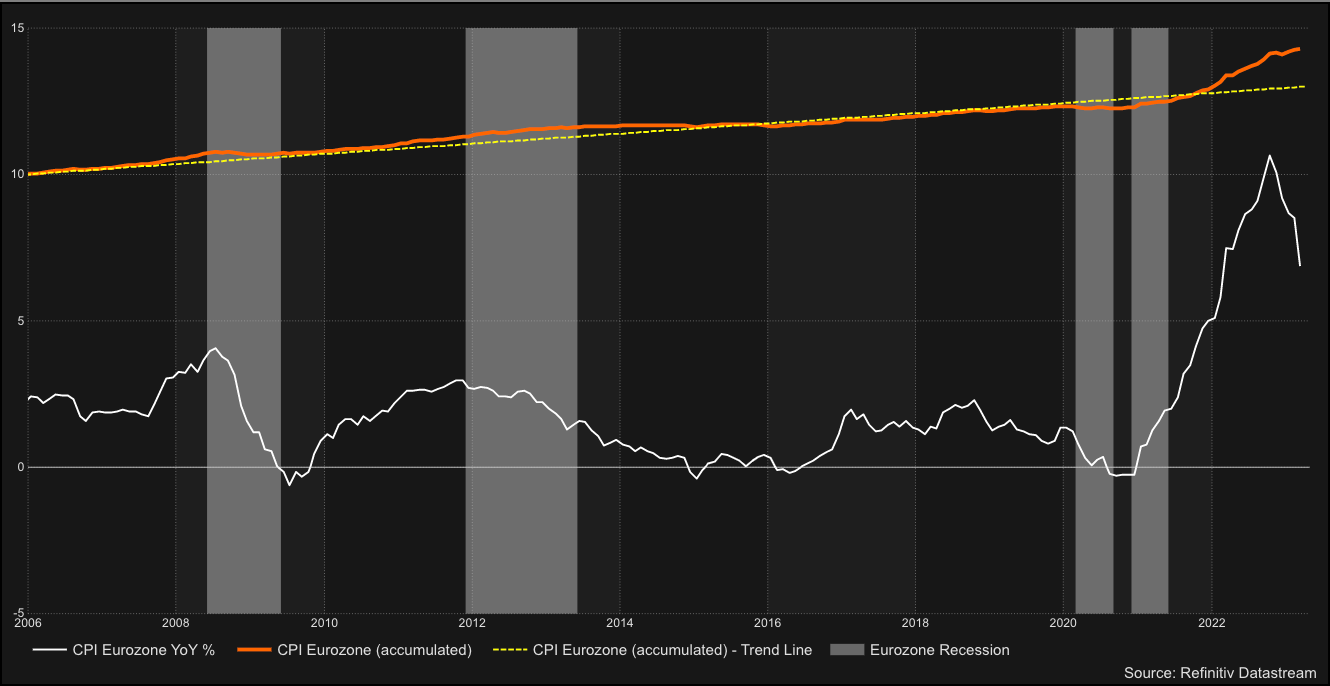

Recently, I came across a chart that drew my attention. Although it may not appear particularly exciting at first glance, it reveals a great deal about the impact of inflation. Many economists, policymakers, and media outlets tend to focus on year-over-year (YoY) comparisons when discussing inflation. However, this chart presents inflation in an accumulative manner, which is also essential to consider.

The YoY chart offers only a snapshot of the changes in consumer prices, while the accumulative chart reveals the longer-term impact of inflation on purchasing power. Inflation is essentially the devaluation of currency or purchasing power, as defined by the European Central Bank (ECB). It occurs when the prices of goods and services increase broadly, reducing the value of currency over time. Therefore, when central banks target an inflation rate of 2% (known as monetary stability), it actually intends to devalue currency by 2% annually. While there are plausible reasons for this, it is paradoxical that we equate this devaluation with monetary stability in our linguistic usage.

To demonstrate the impact of inflation on purchasing power, let's consider the past three years. YoY comparisons can be volatile and not necessarily meaningful for the future. However, in the accumulating model, we can observe the long-term effects of recent price developments. As shown in the overlaid plot, the inflation jump of 2022 reflects a sustained increase in prices in the accumulating model. It highlights the importance of considering both YoY and accumulative charts when examining inflation's effects on purchasing power.

The root causes of last year's price increases are not necessarily relevant in this regard because some of them can be seen as one-off events. What is way more relevant to our long-term purchasing power is the resulting depreciation of purchasing power through the broad based increase of industrial input and consumer prices. As soon as prices rise in the supply chains and affect consumer prices, it is unlikely for them to decline. Historical observations show that once inflation emerges, it persists over time (unless a deep recession intervenes). While this can happen, as seen many times before, monetary and fiscal policies will strive to prevent a deep economic downturn as much as they can.

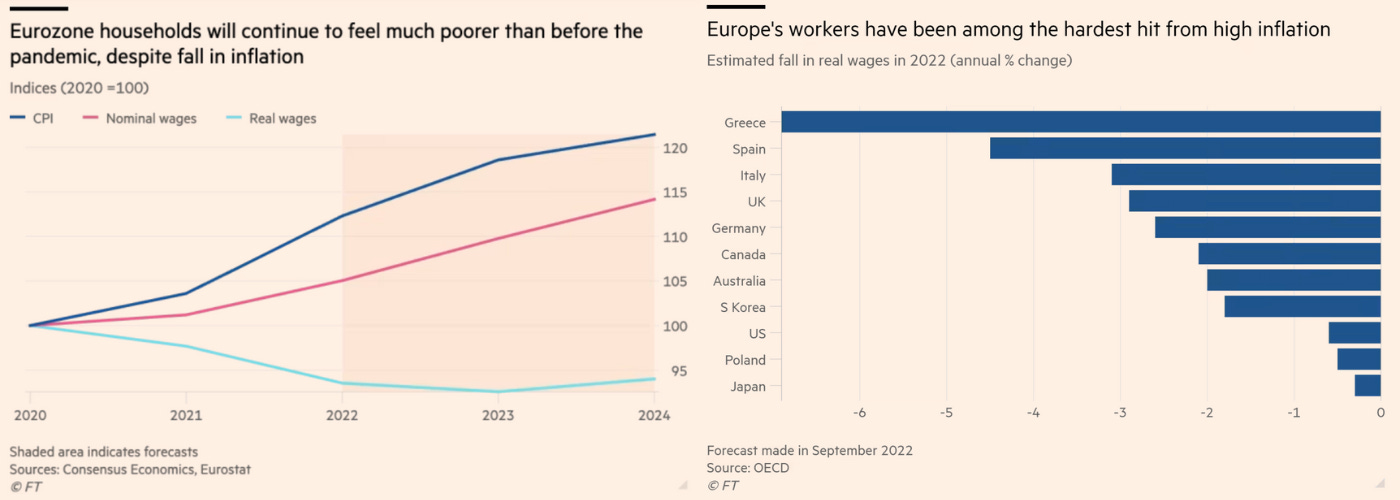

Although investors and consumers might celebrate "falling" inflation to tolerable levels of 4-6 % now, even these “lower” inflation prints are really bad news for consumers. While a 4 % inflation increase may seem small compared to last years 10 % increase, however it actually means that prices have risen by additional 4 % over the long term (in addition to the 10 % increase from last year). This means, that the price level is not only higher for now, it is actually higher forever (as shown in the graph above). This effect leads to a long-term loss of purchasing power of your previously earned money.

Despite the concerning implications of inflation, fortunately there are ways to protect oneself to some extent against loss of purchasing power and currency devaluations. Therefore, it is important to consider safeguarding one's assets before inflation eats up too much of one's nominal wealth. While U.S. central bankers still believe in a successful fight against inflation, others have already resigned and blame the working population for the persistent inflation. Like e.g. Bank of England’s chief economist, Huw Pill:

“So somehow in the UK, someone needs to accept that they’re worse off and stop trying to maintain their real spending power by bidding up prices, whether higher wages or passing the energy costs through on to customers.” See article

Anyhow, inflation affects various segments of the population differently, with winners and losers emerging in these times. Put simply, inflation usually favors debtors and penalizes savers. Debtors benefit as they have accumulated high debts (in the best-case scenario with fixed interest rates) over the past years, and inflation can help them to pay off their debts with less valuable currency. This is because nominal income increases during inflation, while the amount of debt remains the same. However, in order to service one's debts, one must receive an increasing nominal income, which is usually related to the real economy (such as income, uncapped rents, corporate profits, etc.).

While debtors with rising nominal income may enjoy their shrinking debt burden, savers who have invested their money in nominal securities such as savings accounts, bonds, and cash, lose out during inflationary times. As mentioned before, inflation is a loss in the value of the currency, and this loss in value is usually higher than the interest income for savings instruments with long maturities. This effect is resulting in a loss in real wealth of savers.

Typically, retirees are also those with the largest savings balances, while debtors are typically individuals between the ages of 20-50. Due to their circumstances, they have high consumer spending, with the purchase of a home being the largest expenditure in their lives. This mostly happens on the basis of long-term debt. Additionally, most people in this age group are fully employed and directly participate in economic growth, even if real wages do not always rise.

Besides individuals, companies are also an important group of debtors, as they need external capital to grow and invest. Since our economic system is based on a debt money system, they (should) have easy access to credit. In the case of consumer price inflation, companies can benefit from increased prices as long as they keep their costs under control. Although weak business models may perish in the short term, healthy companies can thrive in the long term in such an environment. As the current reporting season shows, large consumer goods groups in particular are currently making use of their pricing power and raising prices significantly.

In addition to certain companies, governments of "rich" well-developed economies with high debt levels and globally well-established currencies are among the inflation winners par excellence. Governments in the U.S., Japan and the Eurozone, in particular, have been borrowing at historically low interest rates from pension funds, central banks, and poorer emerging economies for decades now. For example, China recycles its giant trade surpluses primarily in U.S. and Euro government bonds as official TIC data shows. Instead of defaulting on their debts, countries prefer to devalue their currency because this devalues the real value of their liabilities (as long as these are denominated in their own currencies). Creditor countries get hurt by currency devaluations of their debtors, anyhow they are usually deeply integrated into global supply chains (that is why they produce surpluses) and rising prices in their sales markets might offset the negative impacts. In addition, a weak dollar can also be advantageous for emerging markets occasionally.

In recent years, authorities in "rich" economies have “printed” an excess of nominal money, resulting in huge deficits without much economic growth. This status is unsustainable over a long period of time and so governments have certainly have to intervene. Although higher tax revenues and economic growth are the ideal solutions for reducing deficits in the long term, they are unpopular and difficult to implement. As an alternative, finance ministers may find it more convenient to allow and maintain inflation as a tool for increasing tax revenues indirectly. This occurs as the rising prices of goods, services, and salaries generate more revenue from existing taxation. Austria's Finance Minister Magnus Brunner was surprisingly honest for a politician by explicitly acknowledging this mechanism during a press conference on the first "anti-inflation measures" in 2022.

Moreover, inflation reduces a country's debt level relative to its nominal economic output (debt to GDP ratio). While nominal wages usually rise in accord with nominal GDP, real wages usually remain negative during inflationary regime. In light of this, fiscal policies will likely not interfere too much with rising prices and instead aim to promote nominal economic growth over the next few years.

As previously mentioned, inflationary dynamics do not benefit everyone and the most affected groups are those who are excluded from participating in the real economy. This includes the large group of pensioners who are solely reliant on their statutory pension, which is typically adjusted for inflation with an annual delay. Even those who have diligently saved during their active working lives are usually invested in low-interest securities, such as savings books and bond funds, with the belief that this conservative strategy is prudent and secure. Unfortunately, retirees are now being slowly robbed of their hard-saved money in the last years of their lives.

Considering the increasing number of pensioners in the Eurozone, using financial repression and structurally higher inflation as a solution to cope with the demographic problem in this area seems feasible, but also a little unfair.

If you have made it this far, I thank you for your attention and can reward you with some final thoughts. When making investment decisions it is crucial to consider these dynamics, that are new to many of us. It is therefore important to choose one's investments very wisely. Perhaps this decade, the storytellers who generate actual profits will receive more capital flows, rather than those who are simply burning cash. Throughout history, companies with robust business models that offer scarce goods/services and have pricing power have outperformed nominal assets during periods of structural inflation dynamics. Therefore, higher nominal yields on fixed income do not necessarily protect one's real spending power. In addition, maintaining (monetary) value stability through assets like precious metals, commodities and certain forms of real estate can be beneficial during currency devaluations.

Therefore, given the inflationary environment that we now entered, it is my belief that cash will lose a lot of its value over the foreseeable future, and investing in real assets may be an effective strategy for preserving one's wealth.

DISCLAIMER: The opinions expressed in this report are based on information which Thomas believes is reliable; however, Thomas does not represent or warrant its accuracy. These opinions represent the views of Thomas as of the date of this report. These opinions may be subject to change without notice and Thomas will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities. This is for educational and entertainment purposes only and should not be considered as investment advice.